.png?width=800&height=450&ext=.png "Transitioning to the New CPA Professional Program: Your Questions Answered")

Photo credit: VisualGeneration/Depositphotos.com

In a recent post, I discussed the misinformation about CPA PEP exams and why candidates should not attempt to count Assessment opportunities (AOs) when writing their CPA PEP exams.

Here is a piece of insider information: that post was inspired by a Capstone 2 candidate looking (possibly…) on how to score at the CFE, possibly so they could figure out which user requireds to write (and likely which ones to ignore). I often receive similar candidate queries regarding the module exam, too.

However, in my opinion, the CFE makes it just that much more tempting to try and game the system. Let me explain why…

I can see how a candidate will try to figure out what NOT to do in order to focus on what they CAN do.

That said, the best strategy would be to employ best-case writing tips you have mastered from the modules AND incorporate additional CFE-specific feedback from the Board of Examiner Reports. By doing this, you will ensure, for example, that you write the Situational Analysis (SA) at the beginning of your Day 1 response and then continuously refer back to your SA throughout your response, balance your quants and qual discussion, and provide an overall conclusion in addition to your conclusion for each of the Requireds. Now let us discuss nuances about Days 2/3 of the CFE.

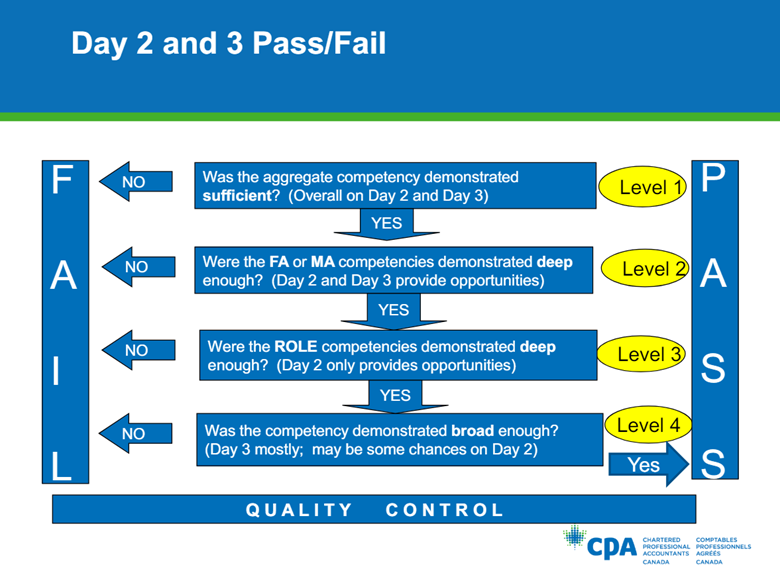

Candidates need to pass each of the 4 levels to pass Days 2/3 of the CFE.

Don’t get “levelled” by Days 2/3 by trying to pick and choose AOs; ignoring AOs to "go for others" is often the culprit of failure, as discussed with unsuccessful candidates. We do not know ultimately what depth and breadth within each AO scoring looks like at the CFE. That is, the bar could be quite low relative to what our expectations are for that particular AO. Ignoring an AO could be ignoring "easy" (relatively speaking) marks.

In my opinion, the above chart depicting the 4 levels required to pass Days 2/3 of the CFE is designed to “catch” anyone trying to pick and choose AOs. This is because, effectively, the CFE is trying to assess what a reasonable CPA would do. In real life, a reasonable CPA would not pick and choose issues to address and items to ignore from clients – this would not be fulfilling our duties as CPAs. As CPAs, we need to have a baseline competence in all six technical competencies and be able to demonstrate those to a reasonable level of proficiency in the time available. In real life, a CPA will likely have more resources (i.e., time, team, and funds to hire external contractors); in an exam scenario, the expectations are scaled down accordingly to reflect the lack of time, time and money to hire external contractors.

Really, the four passing levels reflect that the responsibility of a CPA is to address the user and their needs. Not guess, pick and choose enough issues to get by.

Okay! Well, here are some items that you can avoid counting. In my next article, I will discuss items that I think you should count. Talk soon!

Here is a piece of insider information: that post was inspired by a Capstone 2 candidate looking (possibly…) on how to score at the CFE, possibly so they could figure out which user requireds to write (and likely which ones to ignore). I often receive similar candidate queries regarding the module exam, too.

However, in my opinion, the CFE makes it just that much more tempting to try and game the system. Let me explain why…

CFE Day 1 is marked holistically

This exam is marked “holistically” – meaning a candidate’s response will be looked at in its entirety, at least once, and then evaluated. Candidates will either be “clear pass” or otherwise (i.e., marginal pass, marginal fail, clear fail). All the “clear passes” pass while the remainder are marked again, with any borderline responses (on the Pass/Fail border) marked at least once more.I can see how a candidate will try to figure out what NOT to do in order to focus on what they CAN do.

That said, the best strategy would be to employ best-case writing tips you have mastered from the modules AND incorporate additional CFE-specific feedback from the Board of Examiner Reports. By doing this, you will ensure, for example, that you write the Situational Analysis (SA) at the beginning of your Day 1 response and then continuously refer back to your SA throughout your response, balance your quants and qual discussion, and provide an overall conclusion in addition to your conclusion for each of the Requireds. Now let us discuss nuances about Days 2/3 of the CFE.

Days 2/3 have 4 levels to pass

Candidates need to pass each of the 4 levels to pass Days 2/3 of the CFE.Don’t get “levelled” by Days 2/3 by trying to pick and choose AOs; ignoring AOs to "go for others" is often the culprit of failure, as discussed with unsuccessful candidates. We do not know ultimately what depth and breadth within each AO scoring looks like at the CFE. That is, the bar could be quite low relative to what our expectations are for that particular AO. Ignoring an AO could be ignoring "easy" (relatively speaking) marks.

Diverting energy to counting AOs and Requireds not only could cause a candidate to mis-prioritize but also take away from case writing time. Time that could be spent earning marks and contributing to CFE success.Remember: Your something is better than someone's nothing.

In my opinion, the above chart depicting the 4 levels required to pass Days 2/3 of the CFE is designed to “catch” anyone trying to pick and choose AOs. This is because, effectively, the CFE is trying to assess what a reasonable CPA would do. In real life, a reasonable CPA would not pick and choose issues to address and items to ignore from clients – this would not be fulfilling our duties as CPAs. As CPAs, we need to have a baseline competence in all six technical competencies and be able to demonstrate those to a reasonable level of proficiency in the time available. In real life, a CPA will likely have more resources (i.e., time, team, and funds to hire external contractors); in an exam scenario, the expectations are scaled down accordingly to reflect the lack of time, time and money to hire external contractors.

Really, the four passing levels reflect that the responsibility of a CPA is to address the user and their needs. Not guess, pick and choose enough issues to get by.

Okay! Well, here are some items that you can avoid counting. In my next article, I will discuss items that I think you should count. Talk soon!

Do you have feedback on this post or a question you’d like answered by an experienced CPAWSB educator? Please contact your facilitator or send a question to the General Topic in the Candidate Discussion forum.

Samantha Taylor, PME, CPA, CA

Samantha Taylor, PME, CPA, CA, is an educator and lead policy advisor for CPAWSB and a Senior Instructor of accounting at Dalhousie University. She is on a mission to understand and enable learner efficacy while eliminating doldrums occasionally associated with accounting education. Read more of Sam’s posts at the CPAWSB blog.